- ResiClub

- Posts

- Builders have the most unsold completed homes since 2009—here's where

Builders have the most unsold completed homes since 2009—here's where

Builders are experiencing pricing pressure in certain parts of the Sun Belt—especially in many Florida and Texas markets—where resale inventory has climbed above pre-pandemic 2019 levels.

Lance Lambert

May 02, 2025

Today’s ResiClub letter is brought to you by Stessa!

Track Every Dollar with Stessa—Effortlessly

Managing rental property finances doesn’t have to be a headache. With Stessa, real estate investors can simplify accounting, automate transaction tracking, and stay organized—all in one powerful, easy-to-use platform. Link your bank accounts, property managers, and financial institutions for a clear, accurate financial picture across your entire portfolio.

Stessa also makes bookkeeping stress-free. Track income and expenses by property or portfolio, scan and retrieve receipts on the go, and ensure every transaction is categorized to maximize your deductions. Whether you're managing a portfolio locally or spread out across the country, Stessa keeps you in control from virtually anywhere.

📹 Watch the Demo and see how Stessa can streamline your rental property finances.

✅ Sign Up for Free — Your transactions. Your deductions. Simplified.

Speaking to investors last month, D.R. Horton CEO Paul Romanowski said that the spring 2025 selling season for America’s-largest homebuilder is off to a slower-than-normal start.

“This year’s spring selling season started slower than expected as potential homebuyers have been more cautious due to continued affordability constraints and declining consumer confidence,” Romanowski said on D.R. Horton’s earnings call.

It isn’t just D.R. Horton.

“Demand at the start of this spring’s selling season was more muted than what we have seen historically, despite a healthy level of traffic in our communities. In mid-February, we took steps to reposition our communities to offer the most compelling value, and buyers responded favorably to these adjustments,” KB Home CEO Jeffrey Mezger said on the builder’s March earnings call.

“We do not see the seasonal pickup typically associated with the beginning of the spring selling season,” Lennar co-CEO Jon Jaffe told investors on their March earnings call. “So we continue to lean into our machine focusing on converting leads and appointments and adjusting incentives as needed to maintain sales pace. These adjustments came in the form of mortgage rate buydowns, price reductions, and closing cost assistance.”

Last quarter, Lennar spent the equivalent of 13% of home sales on buyer incentives—up from 1.5% in Q2 2022 at the height of the Pandemic Housing Boom, according to John Burns Research and Consulting. A 13% incentive on a $400,000 home translates to $52,000 in incentives.

This softer housing demand environment has also coincided with an uptick in unsold completed new-builds.

Indeed, since the Pandemic Housing Boom fizzled out, the number of unsold completed U.S. new single-family homes has been rising:

March 2018: 62,000

March 2019: 77,000

March 2020: 76,000

March 2021: 34,000

March 2022: 32,000

March 2023: 70,000

March 2024: 89,000

March 2025: 119,000

The March 2025 figure (119,000 unsold completed new homes) published last week is the highest level since July 2009 (126,000).

Let’s take a closer look at the data to better understand what this could mean.

To put the number of unsold completed new single-family homes into historic context, we created an index: ResiClub’s Finished Homes Supply Index (see chart below).

The index is one simple calculation: The number of unsold completed U.S. new single-family homes divided by the annualized rate of U.S. single-family housing starts.

A higher index score indicates a softer national new construction market with greater supply slack, while a lower index score signifies a tighter new construction market with less supply slack.

If you look at unsold completed single-family new builds as a share of single-family housing starts (see chart below), it still shows we’ve gained slack; however, it puts us closer to pre-pandemic 2019 levels than the Great Recession of 2007–2009.

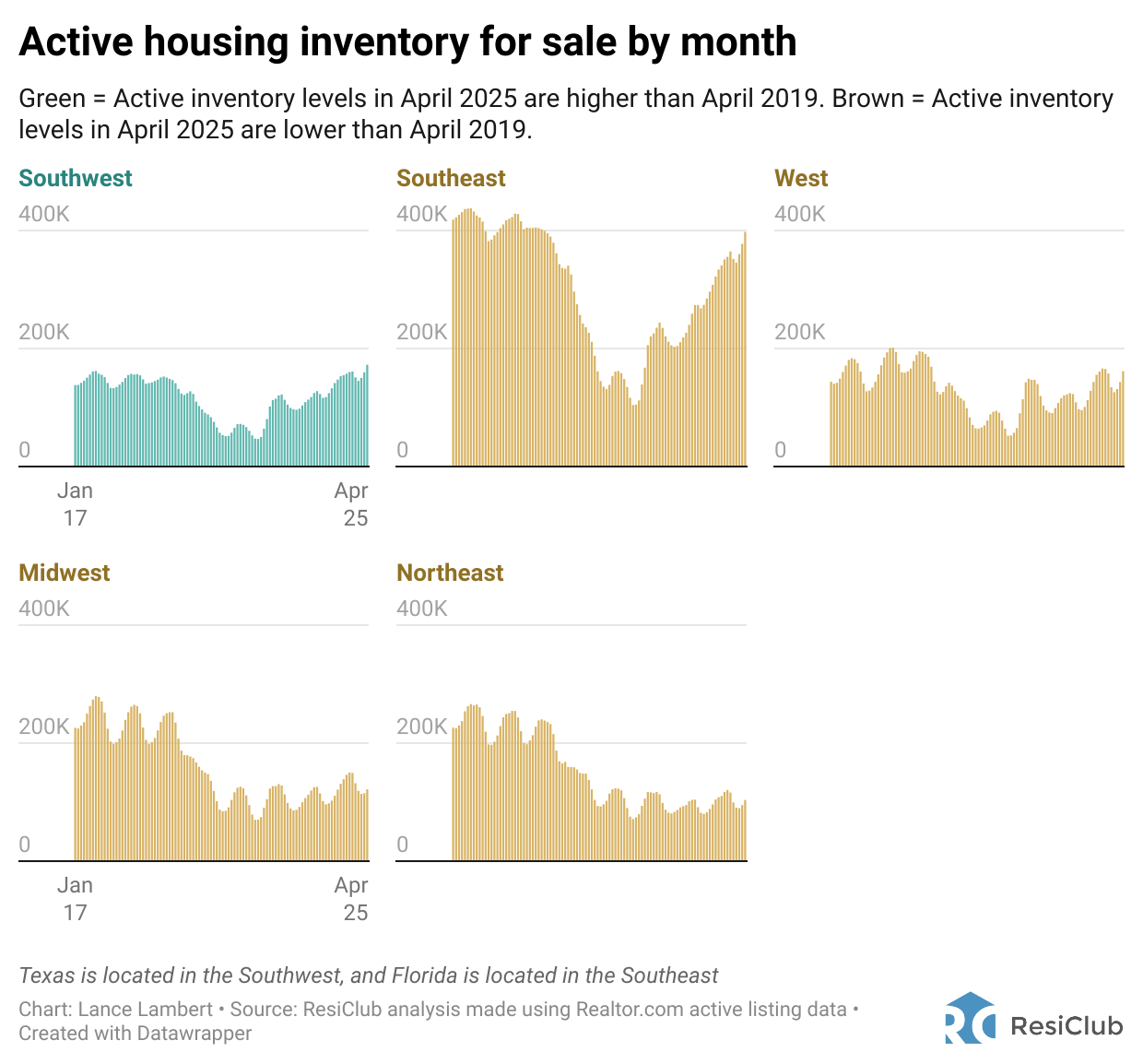

While the U.S. Census Bureau doesn’t give us a greater market-by-market breakdown on these unsold new builds, we have a good idea where they are based on total active inventory homes for sale (including existing homes) that have spiked above pre-pandemic 2019 levels. Most of those areas are in the Sun Belt around the Gulf. Builders are facing pricing pressure in some housing markets, especially in key Florida and Texas markets, where active inventory has jumped back above pre-pandemic 2019 levels.

“I would say in broad terms that Florida was our softest state in terms of sales demand in the first quarter. And because of that, we took the most pricing action there to find the market [in Florida],” KB Home COO Rob McGibney said on the builder’s March 24 earnings call.

“I think you look at our concentration in Texas and through Florida, and certainly when those markets are a little softer, it’s going to cause us to have fewer starts in those markets in response to market conditions,” D.R. Horton CEO Paul Romanowski told investors on April 17, 2025.

Active housing inventory for sale in April 2024 compared to pre-pandemic April 2019 levels:

+19.1% —> Southwest (which includes Texas)

-1.7% —> Southeast (almost there)

-2.7% —> West (almost there)

-41.7% —> Midwest

-51.5% —> Northeast

Unlike many of their peers in Florida and Texas, homebuilders in the Midwest and Northeast have retained more power and haven’t needed to increase incentives as much. Active inventory data matters.

Big picture: There’s greater slack in the new construction market now than a few years ago, giving buyers some leverage in certain markets (in particular in the Sun Belt) to negotiate better deals with homebuilders.

Over the past week, ResiClub PRO members (paid tier) got these 3 additional housing research articles:

Interested in advertising in ResiClub? Email: [email protected]